Article

How Smart Mortgage Brokers Help Australian Property Investors Build Portfolios

A practical guide to how the right mortgage broker helps Australian property investors structure loans, grow a portfolio, avoid cross‑collateralisation and protect borrowing capacity over the long term.

Key Takeaway

A mortgage broker for property investors helps structure loans, select lenders and manage borrowing capacity so Australians can grow property portfolios safely. Lenders typically apply a 3% APRA serviceability buffer and shade rental income to about 70–80%, making strategy more important with each new loan. This article outlines key concepts like cross‑collateralisation, entity selection and rate risk, and finishes with an actionable one‑week plan to engage the right broker.

How Smart Mortgage Brokers Help Australian Property Investors Build Portfolios

A mortgage broker for property investors is a specialist who designs loan structures, selects lenders and manages your borrowing capacity so you can buy and hold multiple properties over time. They focus less on just getting this next loan approved and more on how today’s decision affects property number two, three and four. If you’re serious about building a portfolio, the right broker can easily be the difference between stalling at one property and growing into a resilient, tax‑efficient portfolio.

This guide walks through how investor‑focused brokers think, what they should be doing for you, the traps to avoid (especially cross‑collateralisation), and a one‑week plan to get moving.

1. What an investor‑focused mortgage broker actually does

A lot of brokers can write an investment loan. Far fewer are genuinely skilled at portfolio design.

1.1 Different to a simple home loan broker

For a straightforward first home loan, a good generalist broker might be all you need.

For investors and portfolio builders, your broker’s job expands to:

- Mapping out a 5–10 year property plan, not a one‑off transaction.

- Designing loan structures that keep each property flexible and separable.

- Choosing lenders and products in a sequence that preserves future borrowing power.

- Stress testing your plan against rate rises, vacancies and life events.

If your income, ownership structures or goals are complex, it’s usually worth working with a true specialist. See how this differs in more depth in Specialist vs generalist mortgage brokers: how to decide who you need.

1.2 Key value areas for property investors

An investor‑savvy broker should be adding value in at least five areas:

- Serviceability strategy – understanding how lenders treat existing debts, shaded rent (usually 70–80% of income) and other commitments when you hold multiple properties.

- Equity access – structuring separate loans and limits so you can pull deposits for the next purchase without a full refinance every time.

- Security structure – avoiding unnecessary cross‑collateralisation so one problem property doesn’t drag down the whole portfolio.

- Tax and entity alignment – coordinating with your accountant on personal, company, trust and SMSF structures (without straying into giving tax advice).

- Risk management – buffers, rate strategy, insurance and estate planning basics.

If they’re only talking about rate and not structure, you’re not working with a true portfolio broker.

1.3 When you don’t need a specialist investor broker

You may be fine with a strong generalist if:

- You’re buying one investment property alongside your home loan.

- You’re PAYG with simple finances.

- You don’t plan to hold more than 2 properties in the medium term.

But if you’re self‑employed, using trusts/companies, or your goal is 3+ properties, a specialist investor broker is usually worth it — especially when combined with your accountant and, where needed, a lawyer. For complex income profiles, see also Smarter mortgage broking for self‑employed, professionals and owners.

2. Core lending concepts every investor broker should walk you through

You don’t need to become a credit policy expert. But your broker should explain a few key levers so you can make informed calls.

2.1 Serviceability with multiple properties

Australian lenders assess whether you can afford your loans using a serviceability test, not today’s actual repayments. They typically:

- Assume your loans are charged at your actual rate plus at least 3% (per APRA guidance).

- Use a standard living expense benchmark (HEM) plus your declared spending.

- Count only 70–80% of rental income to allow for vacancies and costs.

Worked example: how rental shading and buffers bite

Say you:

- Earn $160,000 combined PAYG income.

- Own your home: $900,000 value, $500,000 P&I loan.

- Own 1 investment: $600,000 value, $420,000 IO loan, rent $600 per week.

On paper, that rent is $31,200 per year. For serviceability, most lenders will only count $21,840–$24,960 (70–80%). At the same time, they may assess your existing loans as if the rate were ~9% instead of, say, 6% (illustrative only), which can add thousands per month to the test.

A good broker will:

- Model your borrowing capacity across several lenders.

- Show you how choosing P&I vs interest‑only (IO) changes the numbers.

- Plan which debts to reduce first if you’re capacity‑constrained.

2.2 Equity, LVRs and cash‑out for deposits

To grow a portfolio, you’ll usually recycle equity from earlier properties for deposits and costs.

Key concepts:

- Loan‑to‑Value Ratio (LVR) = total loans ÷ property value.

- Most mainstream lenders cap investment loans at 80% LVR without LMI.

- Going above 80% means Lenders Mortgage Insurance (LMI) or a lender cover fee, which increases costs but can help you move sooner.

An investor‑focused broker will:

- Separate your home loan from an investment split used for deposits.

- Arrange a top‑up or separate equity loan rather than a messy full refinance if your current lender is still competitive.

- Flag when it’s worth paying LMI to keep momentum vs waiting and saving more.

2.3 P&I vs interest‑only for investors

Interest‑only loans can improve short‑term cashflow, but they reduce principal slower and are assessed more harshly by many lenders.

Example (illustrative only):

- Investment loan: $600,000 over 30 years at 6.0%.

- P&I repayments ≈ $3,598 per month.

- Interest‑only (for 5 years) ≈ $3,000 per month.

Short term, IO frees up about $600 per month. But:

- After the IO period, repayments jump because the remaining term is shorter.

- Some lenders assess IO loans as if they were P&I over the remaining term, hurting borrowing capacity.

A good broker will show you a side‑by‑side comparison and help you decide which properties (if any) should be IO, and how long, within your risk comfort.

3. Loan structures for portfolio growth: where brokers earn their keep

This is the area most DIY investors and inexperienced brokers get wrong.

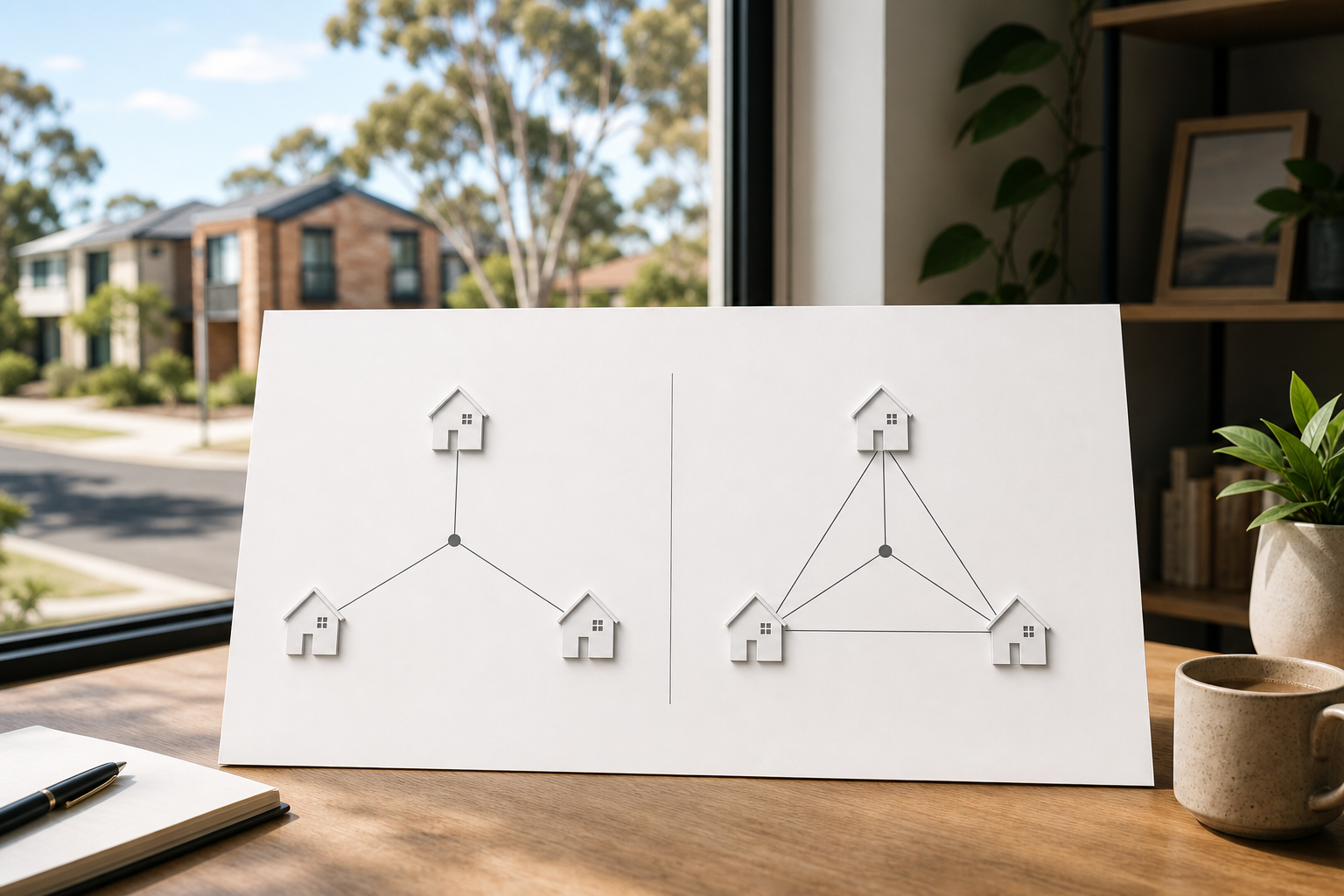

3.1 Stand‑alone securities vs cross‑collateralisation

Cross‑collateralisation is when one lender uses multiple properties to secure one or more loans under a web of mortgages. It can:

- Reduce flexibility to sell or refinance a single property.

- Give the bank more control over your portfolio if values fall.

A stand‑alone structure uses separate loans secured by individual properties (plus targeted equity splits), which is usually safer for portfolio builders.

Structure comparison

| Feature | Stand‑alone security | Cross‑collateralised |

|---|---|---|

| Each property has its own loan? | Yes | Often shared across properties |

| Easier to sell one property without full renegotiation? | Yes | Often no – lender may revalue all |

| Lender can demand debt reduction if values fall? | Less likely | More likely across portfolio |

| Admin when refinancing one loan | Lower | Higher – valuations, legal work on all securities |

| Best use case | Portfolio growth, flexibility | Simple 2‑property cases where never planning to grow |

A careful broker will:

- Explain where cross‑collateralisation already exists.

- Design a path to uncross over time if needed.

- Build new purchases on a stand‑alone basis wherever practical.

3.2 Offsets, splits and debt recycling basics

Beyond structure at the security level, your broker should help design your account and loan splits so you can:

- Park surplus cash in offset accounts to reduce interest while keeping cash accessible.

- Separate deductible (investment) and non‑deductible (home) debt.

- Set up the foundations for debt recycling in concert with your tax adviser.

Example approach:

- Split home loan into Home P&I and Equity IO for investment deposits.

- Link separate offsets to each split to track funds use.

- Over time, direct extra repayments into the non‑deductible home split first.

Your broker shouldn’t be giving tax advice, but they should absolutely understand and support your accountant’s strategy.

3.3 Entities: personal, company, trust, SMSF

Owning investments in entities can help with tax planning, asset protection or succession — but they complicate lending.

Common options:

- Personal names – usually the simplest and most flexible for borrowing.

- Companies and family trusts – can assist with income streaming and asset protection but often have tighter lending criteria.

- SMSFs – use limited recourse borrowing; typically lower LVRs and higher repayments, which can crowd out diversification.

For high‑end or complex portfolios, see How to structure high‑end property purchases the smart way.

A good investor broker will:

- Ask your accountant why a structure is being proposed.

- Explain which lenders support that structure and on what terms.

- Model borrowing capacity with and without entities before you commit.

4. How brokers manage risk for long‑term investors

Property investing is a long game. Your broker should help you manage not just today’s approval, but tomorrow’s shocks.

4.1 Rate cycles and buffers

The RBA cash rate has moved from double‑digits in the early 1990s to 0.10% during COVID, then back up above 4% in recent years. That history shows rates can and do change quickly.

An investor‑focused broker will:

- Model your portfolio at 2–3 percentage points higher than today’s rates.

- Encourage buffers: cash in offset, available redraw, and conservative borrowing.

- Talk honestly about what happens if a major tenant leaves or a reno blows out.

Rather than guessing the future rate path, the focus is: “Would you sleep at night if rates were higher and a property sat vacant for 3 months?”

4.2 Protecting borrowing capacity for your next property

Every decision you make now affects your ability to borrow again later. Your broker should help you:

- Avoid loading up on short‑term consumer debt (credit cards, car loans) that crush serviceability.

- Sequence purchases: often home first, then investments, then SMSF property last if ever.

- Decide when to refinance to a new lender vs stay and top up with the current one.

Sometimes, the right move this year is to consolidate and clean up, not buy. A good reference here is Using a Mortgage Broker to Refinance, Consolidate Debt and Unlock Equity.

4.3 Estate planning, co‑borrowers and guarantees

For portfolio builders, it’s not just about acquiring assets — it’s about what happens if you’re not around.

Your broker should at least raise:

- How loans and ownership are structured between spouses or business partners.

- Whether personal guarantees have been given for company or trust loans.

- The basics of what happens to large home and investment loans if you die, and the importance of your will and insurance aligning with your structure.

For more detail, see How Big Home and Investment Loans Are Handled When You Die. These discussions can feel uncomfortable, but they’re critical if you hold multiple geared properties.

5. One broker for home, investment and business – does it help?

Many portfolio builders are also business owners or self‑employed. The question then is: should one broker handle everything – home loans, investment properties, business facilities and equipment finance?

5.1 The upside of a single, holistic broker

Using one broker can deliver:

- Coordinated strategy – aligning your home, investment and business borrowing so one doesn’t accidentally sabotage the others.

- Clearer story to lenders – one person presenting your overall position and future plans.

- Less duplication – one data set, one set of financials, one point of contact.

This can be powerful if the broker is genuinely strong across home, investment and business lending. Should One Broker Handle Your Home, Business and Equipment Loans? walks through the pros and cons in more depth.

5.2 The risks if they’re not a true specialist

The downside is concentration risk: if that broker is weak in any area, you wear it.

Common issues:

- Over‑use of cross‑collateralisation between home, business premises and investments.

- Business loans structured in ways that hurt personal borrowing capacity.

- Equipment finance taken with the wrong term or balloon, forcing cashflow stress.

A good investor broker will know when to bring in a specialist partner, especially for complex commercial or development finance. They’ll also be transparent on where their expertise stops.

5.3 Self‑employed investors

If you’re self‑employed, your broker has two jobs:

- Present your income in the best possible light within the rules.

- Protect your borrowing flexibility as both a business owner and an investor.

That might mean:

- Choosing lenders who understand company/trust distributions and addbacks.

- Planning loan applications around your tax lodgement timing.

- Coordinating with your accountant before making big changes to how you pay yourself.

For a deeper dive into how this works in practice, read Smarter mortgage broking for self‑employed, professionals and owners.

6. A one‑week action plan to choose the right broker and move forward

You don’t need to solve everything this week, but you can absolutely make meaningful progress.

Day 1–2: Clarify your goals and current position

Write down:

- Your 3–10 year property goals (e.g. 3 properties, $X passive income, or debt‑free home plus 2 investments).

- Your current properties, values, loan balances, rates and repayment types.

- Your income sources (PAYG, business, distributions, bonuses) and major upcoming changes.

This becomes the briefing pack for any broker you speak with.

Day 3–4: Shortlist and interview brokers

Shortlist 2–3 brokers who explicitly work with investors.

Ask them:

- “How do you usually structure loans for portfolio builders?”

- “What’s your view on cross‑collateralisation?”

- “How do you model borrowing capacity across multiple future purchases?”

- “How often do you work with clients who own properties through trusts/companies/SMSFs?”

Compare answers. You’re looking for clear, structured explanations, not buzzwords.

Day 5: Provide documents and get initial scenarios

Once you’ve picked a broker, supply:

- Income evidence (payslips, tax returns, financials if self‑employed).

- Existing loan statements and rates.

- Recent council rates or estimates for property values.

Ask for 2–3 scenarios, such as:

- “What if I buy a $700k investment now using equity from my home?”

- “What if I wait 12 months and pay down $X of home loan first?”

- “How does using a trust or company change my capacity?”

Day 6–7: Decide on a direction – not just a property

Before you rush into a contract, decide on:

- Your preferred loan structure (stand‑alone vs crossed, P&I vs IO).

- A borrowing cap you’re comfortable with under higher rate assumptions.

- A rough sequence for the next 2–3 purchases.

Once you’re comfortable with this higher‑level strategy, you and your broker can move quickly on an actual property knowing the finance is consistent with your plan.

FAQs: Mortgage brokers for property investors and portfolio builders

Do I really need a specialist mortgage broker to buy an investment property?

Not always. For a single, simple investment alongside your home, a strong generalist broker can be fine. Once you plan to hold multiple properties, use entities, or you’re self‑employed, a specialist investor broker is usually worth it. The key is whether they can explain structure, serviceability and strategy clearly, not just quote rates.

How do mortgage brokers get paid for investment loans in Australia?

Most residential brokers are paid a commission by the lender and do not charge you a direct fee, although some specialists may charge for complex work. The commission is broadly similar across mainstream lenders, so a good broker’s focus should be on fit and structure, not which bank pays the most. Always ask your broker to explain how they’re paid and whether any fees apply.

Can a broker help me uncross‑collateralise existing investment loans?

Yes. An experienced investor broker can map your current structures and design a staged plan to separate securities over time. This might involve refinancing some loans, revaluing properties and using equity in one asset to pay down another. It’s often best done gradually, so you’re not hit with unnecessary costs all at once.

How many investment properties can I buy with a broker’s help?

There’s no fixed number; it depends on your income, expenses, existing debts, rental yields and how lenders view your risk profile. A skilled broker can often help you get further than if you went bank‑to‑bank by yourself, mainly through better structuring and lender selection. But they should also be honest about when it’s time to consolidate rather than keep borrowing.

Will using interest‑only loans hurt my ability to grow a portfolio?

Interest‑only loans can help cashflow and sometimes make it easier to hold properties during the early years. However, many lenders now assess IO debts more conservatively, which can reduce borrowing capacity. A good broker will model both P&I and IO scenarios and may recommend a mix depending on your stage, risk tolerance and overall plan.

Can one broker manage my home, investment and business loans together?

They can, and for many investors who own businesses this works well. The broker needs genuine capability across home, investment and commercial lending, and must be disciplined about not over‑crossing securities. If they’re weak in one area, you may be better off with a lead broker who coordinates specialist partners for the other pieces.

Key takeaways

- A mortgage broker for property investors focuses on structure, sequencing and risk, not just approval for the next loan.

- Avoid unnecessary cross‑collateralisation; stand‑alone security structures usually give better flexibility for portfolio builders.

- Lenders apply a 3% buffer and shade rent to about 70–80%, so managing serviceability over time is critical.

- The right broker will coordinate with your accountant and (where needed) lawyer on entities, estate planning and risk.

- You can make real progress this week by clarifying goals, interviewing 2–3 brokers and getting scenarios for your next 1–2 purchases.

If you’re serious about building or restructuring a portfolio, the most valuable step now is a strategy conversation with a broker who genuinely understands investors. Bring your numbers, your goals and your questions — and insist on a long‑term plan, not just a quick approval.

General advice only.

Frequently asked questions

Talk to a CPA-certified broker

Free consultation, plain-English advice tailored to your situation.